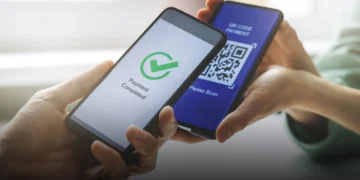

The government’s push to modernise the national payments ecosystem has emerged as a significant finance development for small businesses, with the establishment of a shared digital payments infrastructure aimed at lowering transaction costs and improving interoperability across providers.

In the 2026 Budget Speech, Minister of Finance Enoch Godongwana confirmed that the new payments utility, PayInc, is intended to reshape how digital transactions are processed across the economy.

The move signals a structural shift in the payments landscape, with implications for small retailers, service providers and informal merchants that rely heavily on card and mobile transactions to capture consumer spend.

Merchant fees and fragmented payment systems remain a major cost of doing business for SMEs operating on thin margins. The planned reforms suggest a coordinated effort to create a more integrated payments environment that could gradually improve pricing efficiency and expand access to digital financial services.

Shared payment infrastructure positioned to drive interoperability

In his speech, Godongwana, stated that the payments ecosystem modernisation programme “has achieved its first milestone with the establishment of the payments utility,” confirming that PayInc was completed in November.

Godongwana noted that the platform will provide “open shared digital payments infrastructure to support interoperability across various payment providers, serving as the main platform for high-value and retail transactions.”

This approach is designed to reduce duplication across payment rails and create a common backbone that links banks, fintech firms and payment service providers.

For small merchants, improved interoperability could translate into easier integration of point-of-sale devices, mobile wallets and online payment gateways without the need to manage multiple costly service arrangements.

The reforms are being coordinated by the National Treasury in collaboration with the broader financial sector, reflecting a policy direction that treats payment infrastructure as a core enabler of economic activity rather than a purely private service.

Financial sector reforms extend to crypto and cross-border flows

Alongside payment system upgrades, the budget outlines new draft regulations to bring crypto assets within the capital flow management regime. Godongwana said these measures will complement existing rules aimed at preventing money laundering and fraud, while providing clearer oversight of digital asset transactions.

He added that Treasury is “easing restrictions on the cross-border flows of capital by enabling domestic asset managers to manage portfolios of foreign assets,” a step expected to improve competitiveness and support South Africa’s role as an investment hub on the continent.

For digitally active SMEs, particularly those engaged in e-commerce or cross-border services, these regulatory adjustments could affect how payments are received, settled and reported, potentially altering both compliance requirements and transaction costs.

Payment modernisation tied to broader financial inclusion goals

The budget frames digital payments reform within a wider agenda to ensure the financial sector operates optimally and treats customers fairly. In this context, the payments utility is positioned as a foundational platform to improve efficiency and accessibility across the retail transaction environment.

Godongwana said innovation in digital finance is being prioritised jointly with the central bank, noting that modernising the national payment system is essential for a competitive and inclusive economy. These initiatives are being pursued in partnership with the South African Reserve Bank, which oversees payment system stability and financial sector resilience.